How Snowflake plans to make Data Cloud a de facto standard

Many investors discounted ServiceNow Corporation as Frank Slootman floated the firm, portraying it as something of an improved technical support tool. In reality, the company had a sizable overall market and increased attention within administration of digital solutions, human capital, transportation, safety, advertising, and customer care.

Following the excellent performance under the direction of Chief Executive Slootman as well as Chief Financial Officer Mike Scarpelli, the share price of NOW increased. Predictions were in place when he assumed for Snowflake Inc. that they still repeated the accomplishment, however this time, if nothing else, the business was overpriced right away.

One could argue that, aside from Slootman’s past record of implementation… and statistics, most individuals didn’t truly appreciate the business potential much better today. Good guesses, however most people didn’t realize that Snowflake is creating an information supercloud, as opposed to merely an improved data warehouse, originally described by the business.

We’ll accomplish 4 characteristics throughout this Breaking Assessment and before Snowflake Conference: 1) Go about the current narrative and issues with Snowflake as well as its worth; 2) Convey survey results from Business Research And innovation that almost exactly back up whatever the industry’s CFO is already saying; 3) Express our perspective around what Snowflake has creating, notably its attempt to establish itself the de - facto centralized database; 4) Outline our anticipation for such Snowflake Conference, which will take place near Caesars Palace through Las Vegas scheduled.

Investors anticipate Snowflake to surpass rather than just meet their expectations.

The business essentially met its objectives, which was disappointing news for Snowflake shareholders. Wall Street added to the chorus of disapproval, raising issues with Snowflake’s consumption business model, declining growth figures, lack of sustainability, and value in light of the present macro market circumstances.

After the results, the stock fell less than its IPO price, that, even by route, you really can not touch in each day because the market opened substantially higher. During 2021 and the beginning of 2022, there was a lot of insider selling, which alarmed shareholders. The stock has decreased by over 63 percent so far this year.

However, it’s only true significant shift in the firm’s management over the past quarter was that several of its biggest consumer-facing clients reduced their usage even while increasing. The conversation was not very acrimonious in tone. The inference from certain analysts’ inquiries, however, there’s something intrinsically wrong within Snowflake company, just seems to irritate Scarpelli considerably.

Analyzing the company’s business model of Snowflake:

Let’s start by discussing consumption pricing. In order to better handle unexpected demand variations, one of its investors on the results call questioned Snowflake about the possibility of moving toward a more premium account business model. Scarpelli answered forcefully “NO!” even before the analyzer could complete. It would have been more appropriate for the researcher to question Mike, “Hello Mike, how many of you have thought of changing our pricing scheme and locking your clients in the very same way many older SaaS businesses do… then you could wring more income out of them?

Several of the benefits of a business like Snowflake has been its consumption pricing model, which allows clients, particularly big ones on shifting demand, to reduce usage for tasks that aren’t yet generating revenue.

Let’s move on to insider trading immediately. Insider selling became prevalent in 2017 and will likely continue through 2022. Slootman, Kleinerman, as well as board committee members, traded shares of stock that were highly valuable. at costs of $200, $300, or even $400. Recall that the firm’s worth once exceeded that of ServiceNow and was $1 trillion. that, at this stage of Snowflake’s trip, seems to be just wrong.The cost base for the insiders is frequently in the low single digits. Therefore, in a way, it’s hard to blame people for a present! Because as John Lynch, a legendary investor, once observed, “Insiders purchase with one motive, but can sell for too many.”

However, when the company was trading in the 300s or higher, there wasn’t too much insider buying. It’s important to keep an eye on this pattern. Do insiders currently buy? We’ll continue to watch. Snowflake gives out a lot more stock-based bonuses, and insiders currently control a lot of equity, so it would be possible that they won’t, but we won’t know for sure until future announcements.

Nevertheless, aside from these sizable, consumer-facing businesses, Snowflake’s company has not yet changed considerably.

Updating the model assumptions for 2029 in Snowflake:

Improvements to Snowflake’s financial 2029 projection, which highlight the long-term possibilities the firm sees, were one item Scarpelli accomplished.

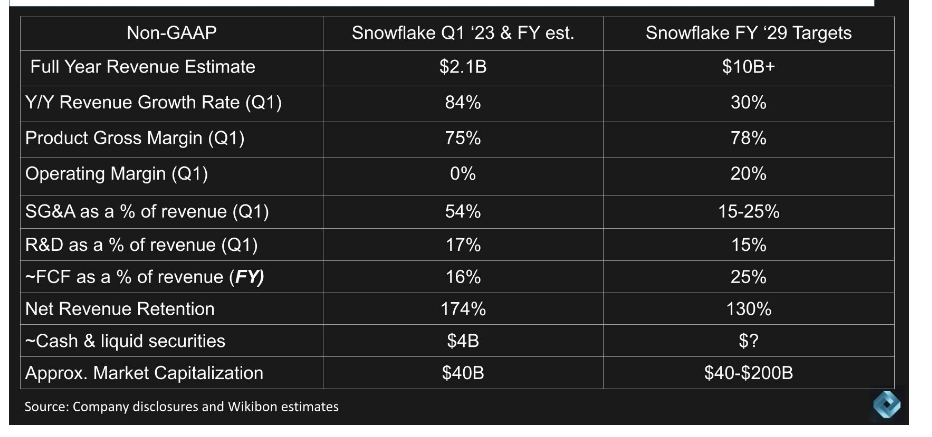

The graph above provides a financial overview of Snowflake’s present operations using data from both quarters and the whole year, as well as a projection of how and why the organization will operate in 2029 depending on the firm’s declarations and our estimations.

Snowflake expects its revenues to exceed 2$billion dollars this year reach $1 trillion or more by 2029. Its pace of growth was 84 percent, and it plans to grow by a sizable 30 percent over the coming years. Operating profits will increase a little, but keep in mind that Snowflake’s price is mostly driven by its clouds expenses because it must spend for its equipment through Aws, Azure, and Google Cloud. However a good goal is the high 70s. Snowflake earnings per share is now quite low, and it wants it to be 20 percent by 2029.You might anticipate that its gearing ratio will allow for significantly lower selling, administrative, and management fees than just the present 54 percent in the coming years. Innovation should remain stable.

Cash flow, though, seems to be the truly interesting metric to follow. Snowflake would generate cash flow at quite a rate of 16% of sales a year, increasing to 25percentage points by 2029, representing $2.5 billion overall FCF, exceeding earlier long-term projections. Additionally, the net income turnover should moderate yet remain above 100%.

Snowflake isn’t about a datastore that you can just throw information inside and deal with later, despite seeing market changes during past seasons from such huge customers . That kind of task will require more flexibility. When you import data using Snowflake, typically specifically intend to generate insights that result in actions and the generation of value.To know more about this cloud data platform, taking up the snowflake training is pretty acceptable.

More elements of the model will be created inside the Snowflake Data Cloud when Snowflake grows its new features, inventions, and ecosystems and provides functionalities to them. By “datasets,” we imply goods and services developed by corporate customers and capable of being paid for immediately, not through analysis but also through controlled information sharing.

Snowflake data cloud as the super cloud platform:

Unlike other cloud-based corporate data warehouses, this Snowflake Data Cloud was developing much beyond that. Snowflake has constructed what is known as a supercloud. This is an advanced feature that includes several capabilities, makes use of another cloud lender’s api and fundamental primitives, and introduces extra value that goes beyond architecture.

Just on the left, this value is shown as compacted turnaround time. This same time it takes a medical business to identify a medicine is sped up by decades in Snow flake example. a wonderful example: There have been a lot more. Snowflake would hasten the delivery of features through organic growth and network expansion. The goal of Snowflake’s Data Cloud would be not to better compete every feature into the system. Instead, it focuses on offering safe, controlled, simple, and effective insights and data.

Conclusion:

Through its community, Snowflake closes holes in its technology and quickens the release of new features. Snowflake intends to establish a de facto norm for data platforms through developing the greatest cloud - based data network in the world in collaboration, safety, management, developer accessibility, intelligent machines, and similar factors.

You could use all the native features once your information has been in the Snowflake Data Cloud.

Article by vivan sai